Unfortunately, little has changed in the Strait of Hormuz so far. It remains closed—and with it, a significant portion of the oil and gas flows on which many countries in Asia and Europe depend remains blocked. Iran is unable to export due to the U.S. blockade, and reports are mounting that there is now barely any storage capacity left to temporarily store the oil being produced. For Tehran, this means a daily loss of revenue of around $470 million. The U.S. government appears to be banking on the Iranian regime running out of financial steam within 15 days at the latest. China would likely be the only obvious buyer—but Beijing, of all places, has no urgent need to step in. Its storage facilities are well-stocked. Nervousness in the rest of Asia—and in Europe as well—is likely to continue rising.

{kind=link}

The U.S., on the other hand, is significantly less affected by the energy crisis. It has its own energy sources, and Wall Street is currently focusing its attention where the action is: high tech. Semiconductors, AI, and quantum computing on one side, and the Q1 results of the Mag-7 companies on the other. Microsoft, Alphabet, Meta, Amazon, and Apple will report their first-quarter results later this week.

{kind=link}

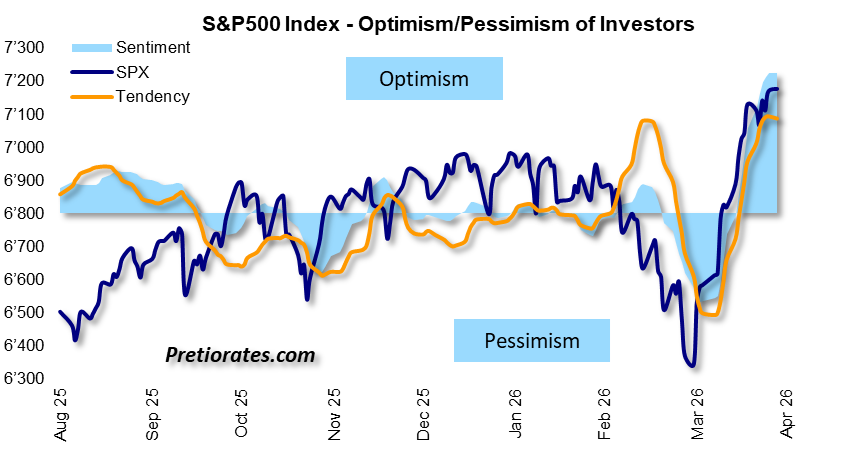

Optimism on Wall Street has reached exceptionally high levels since the low at the end of March. Major corrections are not the usual scenario given such a positive mood, but the coming trading days could well turn into a rollercoaster ride due to corporate earnings. A new development in the Iran conflict would, of course, also have the potential to move the markets. Thanks to the currently robust sentiment, a negative turn is likely to be better absorbed; a positive development, on the other hand, could catapult the indices directly to the next level.

{kind=link}

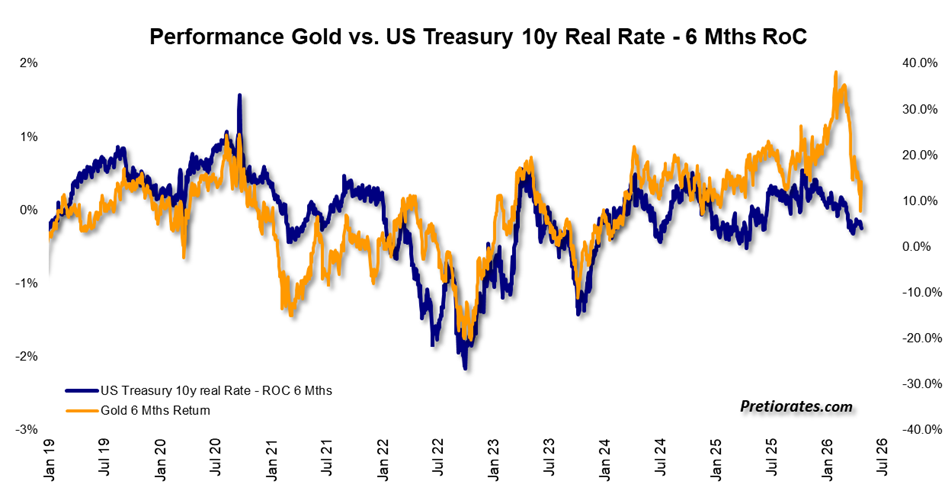

In the case of precious metals, however, there is still no clear trend. Investors remain concerned that high oil prices could trigger new inflation and thus force higher interest rates. In fact, the six-month performance of the gold price has once again converged with the market yield on U.S. Treasuries. This confirms that gold is fundamentally fairly valued at current levels—and that potential upside scenarios are no longer really priced in at this time.

{kind=link}

One of these upside scenarios, as mentioned last week, leads us to the swap market: If higher oil prices were indeed to sustainably fuel inflation and thus lead to higher interest rates, this would also have to be reflected in inflation expectations in the swap market. But it isn’t. Looking five years ahead, there is no significant movement there that points to a higher inflation risk. The clear message from this side is: fears of higher interest rates in the gold market are exaggerated. We’ll know more tomorrow: The U.S. Federal Reserve will certainly comment on this—and that won’t leave the gold market unaffected.

{kind=link}

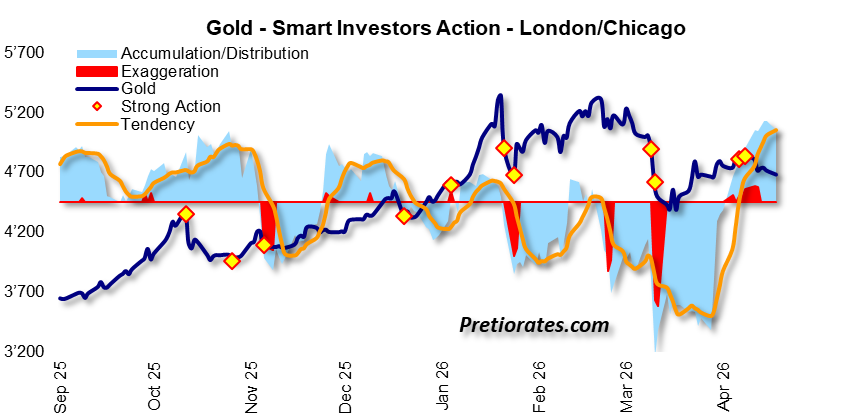

Currently, the market remains divided: on the one hand, the physical market in the East, namely China. There, it appears that Chinese investors have recently been acting rather cautiously. On the positive side, however, the slight dip of the past few days has created an «exaggeration» on the distribution side, as indicated by the red area. This suggests the possibility that demand in Shanghai will pick up again in the near future.

{kind=link}

In the Western paper market, on the other hand, there has recently been strong accumulation; the blue area is clearly on the positive side. However, this demand is not evident in the number of outstanding gold ETFs, where private investors are particularly active. We can therefore assume that professional trading is at work here. This lends fresh credence to rumors that the major bullion banks active in gold trading are building up their long positions.

{kind=link}

The development in the silver market is also interesting, despite the recent lackluster consolidation. While this has not yet been fully reflected in price movements, increased accumulation by «smart investors» has also been evident here in recent weeks.

{kind=link}

Statistics on Chinese silver imports recently caused quite a stir. In March, no less than 836 tons of silver were imported. This corresponds to total global annual production and is no less than 173% above the 10-year average, which stands at 306 tons.

{kind=link}

However, the trend is less bullish than it appears at first glance. Effective April 1, the Chinese government has restored the preferential export tax rate for solar manufacturers to its usual level. It therefore stands to reason that solar manufacturers brought forward their silver purchases to still benefit from the lower export taxes. Accordingly, it can be assumed that China’s silver imports will fall back to a more normal level in April.

{kind=link}

The high demand from China has also been evident since the end of the year in the spread between the silver price in Shanghai and that in the West, which temporarily rose to over 20% at the start of the year. In April, however, since the original higher export tax rate has been reinstated, the spread remained well above 10%. This can certainly be viewed as a positive signal.

{kind=link}

Increased demand from private investors was also frequently cited as a contributing factor. However, this demand is not really evident in the premium of the only silver ETF available in China: the premium has remained at a similar level over the past few months.

{kind=link}

While fears of higher interest rates are likely to continue to somewhat dampen precious metals, a door is opening for silver that actually seemed to have closed again: The war in Iran is not only driving electrification but also boosting demand for non-fossil-fuel-powered vehicles. Demand for EVs literally exploded in several countries in March.

{kind=link}

Therefore, while the bulls in the gold and silver markets may not exactly feel like they’re in a golden age right now, the market could soon rediscover this sector with fresh eyes.